The two wheeler multi-year policy by Liberty General Insurance (LGI) is a unique insurance product brought out especially to offer long term coverage to owners of two wheeler vehicles. Unlike standard annual bike insurance plans, these long term bike insurance plans extend for two or three years.

The main objective behind this insurance policy by LGI is to curb the risk of lapse in policy, and enable people to stay safer while on the road. Longer policy tenures will let people escape the hassles of yearly renewals. Policyholders will also get to enjoy coverage and benefits under this plan by paying the premium in one go.

Loss or damage to the Insured Vehicle

The Company will indemnify the insured against loss or damage to the vehicle insured hereunder and/or its accessories whilst thereon by –

Also if the vehicle is disabled by reason of loss or damage that is covered under the policy, the Company will bear the reasonable cost of protection and removal to the nearest repairer and redelivery to the Insured but not exceeding in all Rs. 300/- in respect of any one accident.

The insured may authorise the repair of the vehicle necessitated by damage for which the Company may be liable under this Policy provided that:

Liability to third parties

Personal accident cover for owner-driver

Subject otherwise to the terms exceptions conditions and limitations of this Policy, the Company undertakes to pay compensation as per the following scale for bodily injury/ death sustained by the owner-driver of the vehicle indirect connection with the vehicle insured whilst mounting into/dismounting from or travelling in the insured vehicle as a co-driver, caused by violent accidental external and visible means which independent of any other cause shall within six calendar months of such injury result in:

| Nature of Injury | Scale of Compensation |

|---|---|

| i) Death | 100% |

| ii) Loss of two limbs or sight of two eyes or one limb and sight of one eye. | 100% |

| iii) Loss of one limb or sight of one eye | 50% |

| iv) Permanent total disablement from injuries other than named above. | 100% |

Provided always that

This cover is subject to

multi-year or a long term bike insurance policy refers to an insurance plan that has tenure of more than one year. Generally a long-term two wheeler insurance tenure is either of 2-3 years.

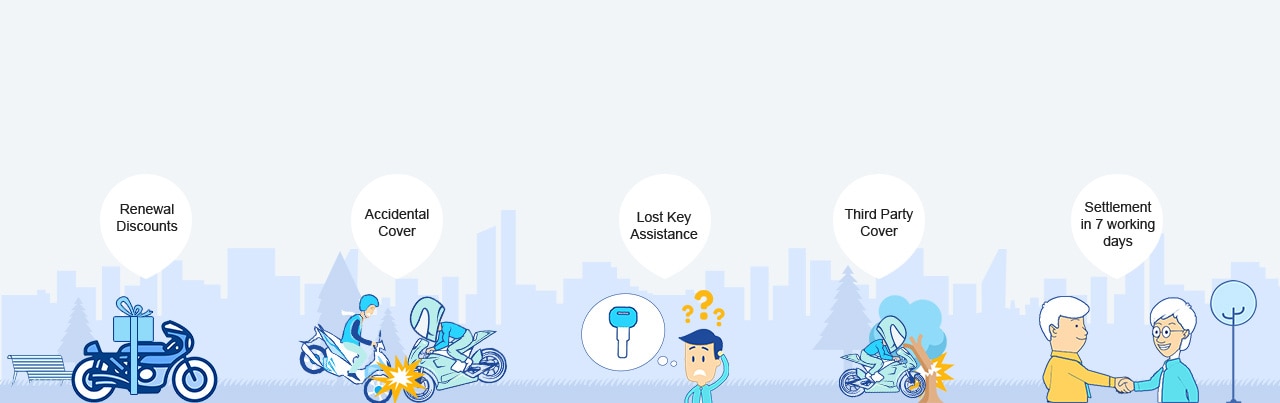

Buying long term two bike insurance policy has various advantages. It saves you from having to renew your bike insurance annually. It also saves you from the annual revisions in insurance premiums every year. You can pay only once and enjoy the coverage for the entirety of your policy tenure. A long term bike insurance policy unlike other standard policies does not cut out on NCBs even if you have made a single claim during your policy tenure.

The term IDV or Insured Declared Value refers to the current market value of the vehicle you are getting insured. This IDV is also the maximum sum insured that you stand to gain in case your vehicle undergoes completely damage or loss. The IDV of vehicles depreciate with each passing year.

In case of long term two wheeler insurance plans, policy buyers can set the IDV of their vehicles within a predefined limit, during the commencement of their policies. Insurers then calculate the age-wise depreciation based on a set rate.

For new two wheelers:-

The premium for your long term bike insurance plan will depend on several factors including –

Yes even if you own an annual bike insurance plan at present, you can switch it to a long-term two wheeler insurance during policy renewal. You will however have to bear the difference in policy premium.

NCB refers to No Claim Bonus and is the benefit that good insurance companies offer to their customers for maintaining their health throughout the year and making no claims.

The advantage of having an NCB is that it is mostly offered in the form of a discount on the premium when you renew your insurance policy. You can thus save good money with an NCB to back you up.

A third party long term two wheeler insurance is a type of multi year bike insurance plan that offers you coverage against expenses arising out of third party claims. This could happen when a third party undergoes damage or loss of property or injury to self, owing to an accident involving your vehicle.

Well comparing the coverage that these plans offers, comprehensive long term two wheeler policies have quite an expansive range. They offer you vehicle damage protection, personal accident cover and third party cover too. Whereas, third party plans are specifically made to protect you against expenses related to third party claims.

But again if you focus on premiums, third party plans are a little cheaper than the prior. So as far as the decision as to which plan is better out of the two, depends very much on the kind of requirement you have.

Some of the scenarios following which you can register a claim under your long term bike insurance plan include –

Thank you very much for your prompt service, While taking insurance from your company, some people told that, if I take insurance from other than dealer, I have to face problem (Like visit to dealer and insurance company surveyor and office, no cashless facility etc) while claim comes, you have pro ven that all those words are wrong and we can take from other than dealar also, I would like to express my please for your service

Thank you very much.As discussed I was feeling helpless because of website OTP issue.But I would like to appreciate your proactive approach to help the customer.Thanks again and wish you a Happy Diwali!!

Average RatingBased on 35 Ratings

I was fed-up with the time-consuming and tiresome insurance renewal process of my previous insurance company, so I...

I never thought I would get my bike insurance renewal done online. But my friend suggested that it’s a better and more...

I just got my bike insurance renewal done online with LGI, and the entire process of renewal was quite easy and convenient...

I found Liberty General Insurance as an excellent option to buy an insurance policy. I recently got my bike insurance...

When you are out on your bike enjoying the soothing wind in your hair, any hitch, be it a flat tyre...

Read More

It has been seen that more and more people prefer investing in two-wheelers rather than four-wheelers, at least ...

Read More

As mandated by the Motor Vehicles Act, 1988, two-wheeler insurance is a must. As an owner of a two-wheeler, many of...

Read More

Chances are that you are among a large number of people who forget to renew their vehicle insurance. Well, there...

Read MoreRegistration Number: 150 | ARN:Advt/2018/March/26 | CIN: U66000MH2010PLC209656

2019 Liberty General Insurance Ltd.

Reg Office: 10th floor, Tower A, Peninsula Business Park, Ganpat Rao Kadam Marg, Lower Parel, Mumbai - 400013

Trade Logo displayed above belongs to Liberty Mutual and used by the Liberty General Insurance Limited under license. For more details on risk factors, terms & conditions please read sales brochure carefully before concluding a sale.

Please provide your details & we will get back shortly.

Are you an existing Liberty General Insurance Customer?*

YES NOI agree to be contacted on my mobile no even if it is registered on NDNC registry